1. Introduction

In an era defined by climate change, resource scarcity, and increasing stakeholder scrutiny, the sustainability of business models is no longer a peripheral concern—it’s a strategic imperative. For decision-makers, investors, and regulators alike, understanding how businesses can create value over the long term while managing environmental and social risks is critical. But while sustainability discussions often focus on ESG (Environmental, Social, and Governance) narratives, the tools for deeply assessing a business model’s staying power are often found in a more traditional domain: financial accounting.

Financial accounting is typically viewed as backward-looking—a record of what has already happened. Yet, embedded within balance sheets, income statements, and cash flow reports are clues about a company’s ability to weather future disruptions, adapt to regulatory pressures, and invest in innovation. When interpreted through the right lens, financial data can help uncover whether a business is genuinely resilient and aligned with sustainable value creation, or simply optimized for short-term gains.

This article aims to bridge the gap between sustainability thinking and financial accounting practice. It provides a structured, step-by-step guide for using financial statements and key accounting metrics to evaluate the long-term viability of business models. Geared toward experts in finance, strategy, and sustainability, the discussion goes beyond surface-level ESG reporting to explore how core financial indicators can serve as proxies—or red flags—for sustainable performance.

Ultimately, this piece argues that financial accounting, when critically applied, is not just about compliance or investor relations. It is a powerful analytical framework for assessing whether a company is truly built to last.

2. Foundations of Financial Accounting in the Context of Sustainability

To evaluate the sustainability of business models using financial accounting, one must first understand the foundational principles of the discipline—alongside its limitations and evolving relevance in today’s sustainability-driven economy.

At its core, financial accounting is the standardized process by which companies record, classify, and report financial transactions. Governed by frameworks like GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards), its primary objective is to provide reliable and comparable information to stakeholders such as investors, creditors, and regulators. Traditionally, this information focuses on financial performance, profitability, and liquidity. However, these metrics were never designed to assess the long-term environmental or social consequences of business activities.

That said, financial accounting still offers a powerful lens for evaluating sustainability—if used with critical nuance. For instance, trends in capital expenditure, debt management, or inventory turnover can reveal much about how a company prioritizes resilience and resource stewardship. The durability of assets, quality of earnings, and consistency of cash flows offer signals about the long-term viability of a firm’s operating model. The challenge lies in recognizing that not all value—or risk—is captured on the balance sheet.

This is where traditional accounting shows its limitations. Many sustainability-related factors—climate risks, human capital management, biodiversity impact—remain off-balance sheet or are disclosed in qualitative ESG reports rather than in core financial statements. Intangible assets such as brand equity, customer trust, or a culture of innovation may only be partially reflected in financial disclosures, if at all. This disconnect can result in underappreciated risks or overvalued assets from a sustainability standpoint.

Recognizing these gaps, leading practitioners and regulators have begun to explore integrated frameworks that bridge financial accounting with sustainability disclosures. Initiatives like the International Sustainability Standards Board (ISSB), SASB, and TCFD represent efforts to standardize this convergence, aiming to make sustainability risks and opportunities visible through a financial lens.

In short, while financial accounting may not offer a complete picture on its own, it remains an essential foundation. By understanding both what it captures and what it omits, analysts can begin to use financial data not just to describe past performance—but to question the future integrity of business models in an uncertain world.

3. Understanding Business Model Sustainability

Before diving into financial metrics, it’s essential to clarify what we mean by a sustainable business model. The term is often used interchangeably with ESG performance or corporate responsibility, but it encompasses a broader and more integrated concept: the ability of a business to create, deliver, and capture value over the long term without depleting the natural, social, or economic systems it depends on.

A sustainable business model goes beyond profitability. It addresses how a company maintains its revenue streams and cost structures in a way that aligns with the evolving expectations of stakeholders—including customers, employees, regulators, and communities. It considers how a firm adapts to external pressures such as climate change, shifts in resource availability, labor conditions, and changing societal norms. In short, it answers a simple but critical question: Can this business thrive—not just survive—ten years from now, and under what conditions?

This sustainability is multi-dimensional. Economically, a company must generate sufficient returns to remain viable and attract capital. Environmentally, it must operate within planetary boundaries, reducing its dependence on finite resources and minimizing its ecological footprint. Socially, it must contribute to, rather than exploit, the communities and workers it engages with. These dimensions are interdependent—poor social practices often lead to regulatory or reputational costs; environmental negligence can lead to supply chain disruptions or stranded assets.

What distinguishes sustainable business models is not merely the presence of ESG initiatives but the structural integration of sustainability into the core of how value is created. For instance, a circular economy approach, where products are designed for reuse and materials are continuously repurposed, embeds sustainability into both strategy and operations. Similarly, a company that aligns executive incentives with long-term impact rather than quarterly earnings is reinforcing sustainability at the governance level.

Understanding these structural elements is key because they eventually show up—or fail to show up—in financial performance. When sustainability is embedded in the business model, financial statements tend to reflect more stable cash flows, lower volatility, and fewer contingent liabilities. When it’s bolted on as a marketing effort, the financial risks tend to accumulate just below the surface.

4. Linking Financial Metrics to Business Sustainability

While sustainability is often discussed through qualitative narratives, financial accounting provides a set of concrete metrics that can be used to assess the underlying health and resilience of a business model. Financial metrics are not only indicators of past performance—they can reveal patterns and priorities that suggest how well a business is positioned to sustain value creation over time. The key is interpreting these metrics through a sustainability lens.

Cash Flow Analysis and Long-Term Solvency

Cash flow is perhaps the most telling indicator of sustainability. A business may report strong earnings, but if it consistently fails to generate operational cash flow, its long-term viability is questionable. Sustainable businesses typically show healthy, recurring cash flows from core operations. These flows support reinvestment in innovation, debt service, and returns to shareholders—without relying heavily on financing or asset sales.

Moreover, free cash flow—the amount remaining after capital expenditures—offers insight into whether a business can grow while maintaining liquidity. Negative free cash flow, if sustained, might signal overinvestment, poor capital discipline, or operational inefficiencies that erode resilience.

Capital Structure and Financial Resilience

How a business finances its operations plays a critical role in its ability to withstand shocks. A highly leveraged company may appear profitable in good times but becomes vulnerable to downturns or rising interest rates. Debt ratios such as debt-to-equity and interest coverage help assess this fragility.

Sustainable models tend to maintain prudent leverage levels and access to diverse funding sources, including green bonds or sustainability-linked loans. These instruments not only improve resilience but also indicate a company’s alignment with environmental and social goals through performance-linked covenants.

Return on Invested Capital (ROIC) vs. Cost of Capital

ROIC is a powerful tool for understanding whether a business is creating or destroying value. A company that consistently earns returns above its cost of capital demonstrates not just efficiency but long-term economic viability. In a sustainability context, high ROIC may also indicate strategic investments in innovation, resource efficiency, and intangible assets like brand trust and intellectual property.

When sustainability is embedded in capital allocation decisions—through low-carbon transitions or regenerative business practices—it often reflects in improved ROIC over time. Conversely, if investments are purely compliance-driven or reactive, returns may lag.

Asset Efficiency and Resource Utilization

Sustainability is tightly linked to how efficiently a business uses its assets. Metrics like asset turnover, inventory turnover, and working capital ratios can highlight whether a company is minimizing waste, managing resources wisely, and avoiding unnecessary capital lock-up.

For instance, companies that adopt circular economy principles often show leaner inventories and higher utilization rates. Similarly, firms with strong digital integration may extract more value from existing assets, reducing the need for capital-intensive expansion.

5. Key Financial Statements and Their Relevance to Sustainability

To assess the sustainability of a business model through financial accounting, one must scrutinize the three core financial statements—balance sheet, income statement, and cash flow statement—not in isolation, but as interconnected narratives of a company’s long-term viability. Each statement reveals different aspects of sustainability when analyzed with intent.

Balance Sheet: Assessing Asset Durability and Liability Risk

The balance sheet offers a snapshot of a company’s financial position at a point in time. For sustainability analysis, particular attention should be paid to the composition and quality of assets and liabilities.

Long-lived assets—like property, infrastructure, or specialized equipment—signal capital commitment. But are these assets adaptable to changing regulations or environmental conditions? For instance, fossil-fuel-based infrastructure may soon become stranded or devalued. Likewise, intangible assets such as goodwill or intellectual property must be scrutinized for real economic value, especially in industries undergoing rapid transformation.

Liabilities also tell a sustainability story. Excessive short-term debt or exposure to contingent liabilities (e.g., environmental fines, litigation) can indicate financial fragility. A sustainable business maintains a balanced, long-term-oriented capital structure and provisions for known future risks.

Income Statement: Quality of Earnings and Value Creation

While the income statement reflects profitability over a period, sustainable value creation is not just about high earnings—it’s about the quality and consistency of those earnings.

Recurring revenue from core operations suggests a stable model, while heavy reliance on non-recurring gains (e.g., asset sales, tax credits) can mask structural weaknesses. Gross and operating margins reveal pricing power and operational efficiency—two indicators of strategic positioning and resilience in competitive or resource-constrained markets.

Additionally, a shift in cost structures—from resource-intensive inputs to service-based models, for example—may reflect a more sustainable approach to value creation and delivery.

Cash Flow Statement: Sustainability of Operational Cash Flows

The cash flow statement translates accrual-based earnings into real liquidity. In sustainability assessments, the operating cash flow is paramount—it indicates whether the company’s core business model is self-sustaining.

CapEx patterns also reveal strategic direction. Investments in R&D, renewable energy, or supply chain modernization reflect a long-term orientation, whereas excessive maintenance CapEx may indicate aging infrastructure or deferred risks. Negative free cash flow isn’t necessarily bad—if it supports future resilience—but the source and context must be evaluated.

Financing and investing activities can also signal sustainability alignment. A shift toward issuing green bonds, reducing reliance on debt, or funding ESG-aligned acquisitions often speaks to the company’s strategic priorities.

Notes and Disclosures: Revealing Hidden Sustainability Risks

The footnotes and management discussion sections, while often overlooked, are critical in understanding non-financial risks that may eventually become material. Disclosures about climate risks, legal proceedings, supplier dependencies, or regulatory exposures can highlight vulnerabilities that aren’t captured in the numbers—yet.

Additionally, the way companies talk about sustainability in their financial reports—whether it’s a boilerplate ESG section or a substantive risk-adjusted strategy—indicates the level of integration and maturity in their approach.

In summary, the financial statements offer a powerful but often underutilized toolkit for sustainability analysis. When viewed collectively and interpreted critically, they provide insight not only into a company’s performance, but its preparedness for a future where sustainability is no longer optional—but foundational.

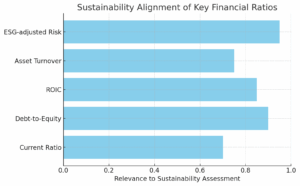

6. Ratios and Indicators for Evaluating Sustainable Performance

Financial ratios condense complex financial data into actionable insights. When viewed through the lens of sustainability, these indicators help assess whether a company’s performance is resilient, efficient, and aligned with long-term value creation. While no single ratio tells the whole story, taken together they can illuminate patterns of strength—or signals of structural risk.

Liquidity and Solvency Ratios

Liquidity ratios such as the current ratio and quick ratio reveal a company’s ability to meet short-term obligations. Sustainable companies tend to maintain adequate liquidity buffers, reducing their vulnerability to economic or environmental shocks that can disrupt operations or revenue streams.

Solvency ratios, such as debt-to-equity and interest coverage, provide insight into long-term financial resilience. Companies with more conservative leverage structures are generally better positioned to absorb volatility from market shifts, regulatory changes, or sustainability-related capital investments. Overleveraged firms may lack flexibility when needed most—such as during a rapid transition to lower-emission operations.

Profitability Ratios in a Sustainability Context

Traditional profitability ratios—gross margin, operating margin, and net profit margin—remain central, but must be contextualized. High margins built on environmentally or socially exploitative practices may be unsustainable, especially as regulation and stakeholder pressure mount. Conversely, modest margins supported by efficiency, transparency, and stakeholder trust may signal a more durable business model.

Return on equity (ROE) and return on assets (ROA) should also be evaluated in terms of how capital is deployed. Are returns driven by sustainable innovation and customer loyalty, or by aggressive cost-cutting and financial engineering?

Efficiency and Turnover Ratios

Ratios like asset turnover, inventory turnover, and working capital turnover measure how efficiently a company uses its resources. In a sustainability context, high efficiency often correlates with lower waste, leaner operations, and more agile supply chains—all crucial for long-term resilience.

For example, a company with a high inventory turnover may be better at responding to market changes and reducing obsolete stock, which in turn lowers environmental impact and capital lock-up.

ESG-Adjusted Financial Indicators

Some firms and analysts now blend traditional ratios with ESG data, creating hybrid indicators such as emissions per unit of revenue, or ESG-adjusted ROIC. While not yet standardized, these metrics reflect the growing need to evaluate financial performance alongside environmental and social impact.

Financial ratios remain indispensable. But for sustainability-focused analysis, their real value emerges when they are interpreted in context—against industry norms, historical trends, and the strategic direction of the business.

7. Integrating ESG Factors into Financial Analysis

The traditional separation between financial performance and environmental, social, and governance (ESG) considerations is rapidly breaking down. For analysts focused on sustainability, the next frontier is the systematic integration of ESG factors into core financial analysis. This integration is not about replacing financial metrics, but enhancing their relevance in a world where non-financial risks are becoming financially material.

Understanding ESG Reporting Frameworks

A growing number of frameworks now guide companies in disclosing ESG-related information in a structured and comparable way. Standards like the Sustainability Accounting Standards Board (SASB) focus on sector-specific financial materiality, while the Global Reporting Initiative (GRI) emphasizes stakeholder impact. The Task Force on Climate-related Financial Disclosures (TCFD) highlights climate-related risks and opportunities, particularly as they affect financial planning.

Recently, the creation of the International Sustainability Standards Board (ISSB) under IFRS Foundation marks a significant step toward globally harmonized ESG reporting. These frameworks are beginning to feed into financial reports themselves, particularly in the management discussion & analysis (MD&A) section and footnotes.

Mapping ESG Data to Financial Accounting

The key to meaningful integration lies in linking ESG factors to financial outcomes. For example:

- A company with high carbon emissions faces transition risks (e.g., carbon taxes, regulation) that could affect future operating costs and capital expenditures.

- Poor labor practices can lead to high turnover, low productivity, or litigation—impacting cost structures and liabilities.

- Weak governance increases the risk of misreporting, strategic drift, and reputational damage—all of which may manifest in volatility of returns or higher cost of capital.

Integrating ESG means translating such risks and opportunities into assumptions used in financial models—adjusting discount rates, altering revenue growth expectations, or reevaluating asset lifespans.

Challenges to Integration

Despite growing momentum, integration remains difficult. ESG data is often:

- Non-standardized: Different companies report on different metrics, with varying methodologies.

- Unaudited: Much ESG data lacks the rigor of financial audits, undermining its reliability.

- Lagging: There’s often a time delay between ESG practices and their financial impact.

Analysts must therefore balance skepticism with strategic foresight—identifying which ESG factors are truly material and how they may evolve over time.

Tools and Approaches

Advanced practitioners increasingly use:

- Scenario analysis (e.g., for climate stress testing)

- Sustainability risk scoring systems

- Multi-capital models (e.g., integrating natural, human, and financial capital)

Some integrate sustainability-adjusted DCF models that reflect long-term ESG risks in terminal value assumptions or cost of capital inputs. Others overlay ESG scores onto financial ratios to weight portfolio risk.

Integrating ESG into financial accounting is not about checking boxes—it’s about capturing a fuller, more accurate picture of business reality. In a world where long-term viability is tied to environmental and social dynamics, this integration is no longer optional—it’s the new baseline for credible analysis.

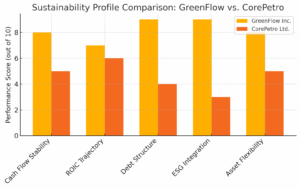

8. Case Study: Assessing the Sustainability of Two Contrasting Business Models

To illustrate how financial accounting can be used to assess business model sustainability, let’s compare two hypothetical—but realistic—companies operating in the same industry: GreenFlow Inc. and CorePetro Ltd., both active in the energy sector.

Company Profiles

- GreenFlow Inc. is a renewable energy firm focused on wind and solar generation. It has a capital-light model, heavily investing in R&D and digital optimization of energy grids. The company reports under IFRS and integrates SASB-aligned ESG disclosures in its annual report.

- CorePetro Ltd. is a conventional oil and gas producer with a long-standing infrastructure base. It has strong current cash flows but limited diversification. ESG disclosures are minimal and primarily reactive, included in a separate sustainability report.

Balance Sheet Analysis

GreenFlow’s asset base is heavily weighted toward intangible assets and short-lived equipment. However, its liabilities are well structured, with green bonds representing 40% of its debt and favorable interest rates tied to emissions targets. CorePetro, on the other hand, has significant long-term fixed assets that may face devaluation under future climate policy. Its liabilities include high-interest debt tied to legacy infrastructure investments.

From a sustainability standpoint, GreenFlow’s balance sheet shows strategic flexibility, while CorePetro’s fixed capital and long-term obligations could become financial burdens.

Income Statement and Cash Flow Trends

GreenFlow’s income statement reflects moderate but growing revenues, with positive operating income. Margins are lower, partly due to upfront R&D costs, but consistent reinvestment signals a future-oriented model. Operational cash flow is positive and reinvested into expansion and innovation.

CorePetro reports high net income and strong cash flow—typical of the fossil fuel sector during favorable market conditions. However, a closer look shows substantial reliance on asset sales and tax deferrals to maintain profitability. Its CapEx is primarily for maintenance, not innovation.

Here, GreenFlow exhibits lower but more sustainable profitability, while CorePetro’s earnings quality is susceptible to commodity cycles and policy shifts.

Key Ratios and Indicators

GreenFlow’s ROIC is close to its cost of capital but improving annually. Its debt-to-equity is low, and ESG-adjusted risk scores are favorable. Inventory turnover is high, reflecting lean operations.

CorePetro has a high ROE, but this is partly inflated by leverage and asset write-down reversals. Its interest coverage ratio is weakening, and there is no integration of ESG performance into executive compensation or financial planning.

Strategic Implications

While CorePetro currently outperforms financially, its model is underpinned by declining assets and external risks. GreenFlow shows a slower, but structurally sound trajectory supported by reinvestment, stakeholder alignment, and adaptability.

This contrast illustrates a central insight: financial performance must be evaluated through the lens of strategic resilience. When sustainability factors are integrated into financial analysis, it becomes easier to differentiate between models that are merely profitable today—and those built to thrive tomorrow.

9. Emerging Trends and Innovations in Sustainable Financial Accounting

As sustainability becomes a core strategic concern for businesses and investors alike, financial accounting is evolving to better reflect long-term value and risk. Several emerging trends are reshaping how sustainability is embedded into financial reporting and decision-making.

1. Integrated Reporting

A key innovation is the rise of integrated reporting, which aims to unify financial and non-financial disclosures into a cohesive narrative. Rather than separating ESG data into standalone reports, integrated reports connect sustainability performance directly to financial outcomes. This holistic approach, promoted by frameworks like the <u>Integrated Reporting Framework (<IR>)</u>, allows stakeholders to assess how environmental and social issues influence capital allocation, business strategy, and long-term profitability.

2. Digitalization and AI in Financial Analysis

Advanced technologies—especially AI, machine learning, and big data analytics—are transforming how sustainability risks are identified and quantified. Analysts can now scrape and model unstructured data (e.g., supply chain emissions, news sentiment, satellite imagery) and correlate it with financial outcomes. These tools enhance forward-looking risk assessment and can flag material ESG issues long before they surface in financial statements.

3. Real-Time, Dynamic Disclosures

Regulatory momentum is shifting toward more frequent and dynamic disclosures. Quarterly ESG updates, scenario-based stress testing (e.g., climate transition impacts), and real-time risk dashboards are emerging, especially among large multinational firms and financial institutions. These developments improve transparency and reduce information lag for investors.

4. Evolving Regulatory Standards

Regulators are rapidly advancing requirements to integrate sustainability into mainstream financial reporting. The European Union’s Corporate Sustainability Reporting Directive (CSRD) and global efforts by the ISSB are pushing companies toward more standardized, audit-ready ESG disclosures that sit alongside traditional financial metrics.

These trends reflect a growing recognition: the tools of financial accounting must evolve if they are to remain relevant in a world where sustainability is not a niche concern, but a core driver of business success and systemic stability.

10. Conclusion and Recommendations

Sustainability is no longer a peripheral concern—it’s central to business survival and success. While ESG narratives and impact assessments have gained prominence, financial accounting remains one of the most rigorous and widely understood tools for evaluating long-term viability. When interpreted with a sustainability lens, financial statements and metrics provide crucial insight into whether a business model is resilient, adaptable, and truly built to endure.

This article has outlined a framework for experts to assess sustainability using financial accounting—from cash flow health and capital structure to the nuances of financial statement analysis, ESG integration, and emerging trends. The message is clear: sustainability and financial performance are not separate domains. They are increasingly intertwined.

Recommendations:

- Integrate ESG into financial modeling: Treat sustainability-related risks and opportunities as financially material, adjusting assumptions accordingly.

- Prioritize quality over quantity in disclosures: Focus on consistent, decision-useful ESG data that links clearly to financial outcomes.

- Adopt a forward-looking mindset: Use scenario analysis, adjusted DCF models, and early-warning indicators to anticipate long-term risks.

- Push for harmonized reporting standards: Support convergence around ISSB, SASB, and TCFD frameworks to improve comparability.

For CFOs, analysts, and sustainability professionals, financial accounting is not just a backward-looking tool—it’s a forward-looking lens on the sustainability of business models in a volatile world.