1. Introduction: Why SOX 2.0 Is on the Radar

More than two decades after the passage of the Sarbanes-Oxley Act (SOX) in 2002, the phrase “SOX 2.0” is surfacing in boardrooms, audit committees, and legal circles with increasing frequency. While there is no formal legislation bearing that name—yet—the convergence of regulatory signals, market pressure, and evolving corporate risk has given rise to serious discussions about whether we’re heading toward a new era of compliance mandates.

The original SOX emerged from the rubble of corporate scandals—think Enron, WorldCom, and Tyco—that exposed glaring weaknesses in financial oversight. Its provisions reshaped corporate governance, internal controls, and executive accountability. But fast-forward to today’s landscape, and the threats have evolved. We’re no longer just talking about earnings manipulation or audit failures. Today, data breaches, ESG misstatements, and algorithmic bias can inflict just as much reputational and financial damage.

Recent high-profile enforcement actions, coupled with the SEC’s push for greater disclosure around cybersecurity and climate risk, suggest that regulators are rethinking what transparency and control mean in the 21st century. At the same time, lawmakers and institutional investors are calling for corporate responsibility that goes beyond financial reporting.

Is this the beginning of a regulatory “act two,” or just a tightening of the bolts on the original framework? That’s what this article aims to unpack—step by step. We’ll cut through the noise to examine the drivers behind the “SOX 2.0” conversation, distinguish rumors from real policy shifts, and offer a grounded analysis of what may lie ahead for companies, executives, and compliance professionals alike.

2. The Original SOX: Legacy, Gaps, and Lessons

To understand the potential shape of a “SOX 2.0,” it’s essential to revisit the intent and impact of the original Sarbanes-Oxley Act. Enacted in 2002 in response to some of the most egregious corporate accounting scandals in U.S. history, SOX was designed to restore investor confidence by imposing strict reforms on financial disclosures, internal controls, and executive accountability.

At its core, SOX brought structure and rigor to the previously inconsistent world of corporate governance. Section 302 required CEOs and CFOs to personally certify financial statements, introducing a new layer of executive liability. Section 404, perhaps the most impactful (and burdensome), mandated management and external auditor assessments of internal control over financial reporting. It also led to the birth of the Public Company Accounting Oversight Board (PCAOB), which redefined the auditing landscape.

Despite initial backlash over cost and complexity, SOX has become ingrained in public company operations. It is credited with significantly improving audit quality, reducing earnings management, and fostering a culture of accountability in financial reporting. However, it was never a catch-all.

Table: Key Provisions of SOX (Selected)

| Section | Focus Area | Summary |

|---|---|---|

| 302 | Corporate Responsibility | Executive certification of financial reports |

| 404 | Internal Controls | Management and auditor assessments of controls |

| 802 | Criminal Penalties | For altering or destroying financial records |

| 906 | Criminal Certification | CEO/CFO certifications with criminal liability |

Gaps and Limitations

What SOX didn’t anticipate were the future vectors of risk. Cyber threats, data integrity, algorithmic decision-making, ESG claims, and even third-party risk—all now touch corporate reputation and investor trust as deeply as misstatements once did. SOX was tightly focused on financial reporting and audit-related governance. But today’s risk landscape is broader, faster-moving, and increasingly non-financial in nature.

Moreover, critics argue SOX inadvertently created a compliance culture overly reliant on checklists and documentation. While it helped standardize practices, it didn’t necessarily strengthen the strategic thinking around enterprise risk or encourage agility in evolving governance frameworks.

As these limitations become more apparent, especially under new pressures from regulators and markets, the call for a “modernized” or extended version—what many are calling SOX 2.0—is gaining credibility.

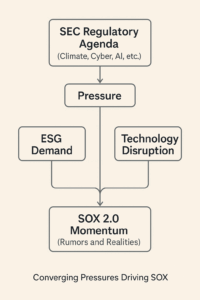

3. Emerging Pressures Driving Talk of “SOX 2.0”

While there’s no bill labeled “Sarbanes-Oxley 2.0” moving through Congress (yet), the conditions for a new compliance paradigm are ripening. The push isn’t coming from one direction—it’s a confluence of regulatory expansion, market expectations, technological disruption, and public scrutiny. Together, they’re creating the kind of systemic pressure that preceded the original SOX.

1. The SEC’s Expanding Agenda

The Securities and Exchange Commission has taken a markedly more assertive stance under current leadership. Recent proposals demand greater transparency in climate-related disclosures, cybersecurity governance, and the use of AI in financial decision-making. These are not fringe issues—they cut to the core of what stakeholders now view as “material risk.”

For instance, the SEC’s proposed climate rule would require public companies to disclose Scope 1, 2, and in some cases, Scope 3 emissions—alongside climate-related governance structures and risk management processes. Similarly, new cyber risk disclosures would force companies to detail board oversight, material incidents, and response readiness.

2. ESG and Investor Activism

Environmental, Social, and Governance (ESG) expectations are shifting from voluntary guidelines to quasi-regulatory standards. Institutional investors such as BlackRock and Vanguard are demanding standardized ESG disclosures, while shareholder activism is targeting boards that fail to act on climate, DEI, or ethical sourcing. Failing to address these issues can trigger not just reputational harm but actual capital flight.

3. Tech Risk and AI Accountability

The rapid integration of artificial intelligence into corporate operations introduces a new class of risk—opaque, fast-evolving, and difficult to audit. Regulators and watchdogs are beginning to question the lack of oversight over algorithms that impact credit decisions, trading, and customer segmentation. In many ways, this echoes the lack of understanding that auditors once had of off-balance-sheet entities in the early 2000s.

4. Public Trust and Political Signals

Beyond markets and regulators, the public is less tolerant of perceived corporate irresponsibility. Whistleblower reports and social media virality can catalyze legal and regulatory responses within days. On Capitol Hill, both parties have floated proposals around expanding executive accountability and tightening disclosure standards—especially in the wake of high-profile collapses like FTX and Archegos.

Diagram: Converging Pressures Driving SOX 2.0 Conversations

These forces aren’t operating in isolation—they’re accelerating each other. The line between “voluntary best practice” and “regulatory requirement” is increasingly blurry. Whether SOX 2.0 arrives as a sweeping new law or a series of incremental rules, the trajectory is clear: compliance expectations are growing more complex, and more existential.

4. What’s Actually Happening? Separating Rumor from Regulation

As the drumbeat around “SOX 2.0” grows louder, it’s important to separate media-fueled speculation from grounded regulatory developments. While headlines often leap to sweeping conclusions—“New SOX Bill Incoming!” or “SEC to Mandate ESG Audits”—the real picture is more nuanced. Yes, there is momentum for expanded compliance, but the form it’s taking is evolutionary, not revolutionary—for now.

A Patchwork, Not a Package

Unlike the original SOX, which arrived as a comprehensive piece of legislation in the aftermath of corporate scandal, today’s compliance wave is more fragmented. Most of the current changes are coming via regulatory rulemaking, particularly from the SEC, rather than through congressional action.

For example, the SEC’s climate disclosure proposal and its finalized cybersecurity incident disclosure rule represent significant expansions of what companies must report—but they aren’t part of a new “SOX Act.” They build on existing securities law frameworks, particularly the 1934 Exchange Act, rather than create an entirely new legal apparatus.

What the SEC Is Doing

- Cybersecurity Risk Governance (Final Rule, 2023): Requires companies to disclose material cybersecurity incidents within four business days and describe board oversight and risk management processes.

- Climate Risk Disclosure (Proposed Rule, pending): Would mandate detailed disclosures on emissions, governance, and climate-related risks, especially for large filers.

- AI and Predictive Technology Disclosures (Under Study): The SEC has issued requests for comment on how companies use AI in decision-making, especially in investment and lending contexts.

Meanwhile, industry watchdogs and accounting standard-setters are also signaling shifts. The PCAOB is increasing its focus on audit firm independence and fraud detection, and the Financial Accounting Standards Board (FASB) is exploring guidance for disclosure of intangible risks.

Table: Rumors vs. Reality – SOX 2.0 Compliance Landscape

| Rumor | Reality |

|---|---|

| Congress is drafting “SOX 2.0” legislation | No bill exists. Changes are driven by SEC rulemaking and PCAOB updates. |

| ESG audits will become mandatory next year | No mandate for ESG audits yet; voluntary frameworks dominate. |

| CEOs will face criminal penalties for ESG misstatements | No criminal statutes have changed; liability tied to material misstatements |

| All companies must disclose carbon emissions | Only large registrants under the proposed SEC rule, and even then, phased. |

| SOX 404 is expanding to cover cybersecurity | Cyber rules are separate from SOX, but internal control practices may adapt. |

A Moving Target

The term “SOX 2.0” is often used as shorthand—a placeholder for a perceived shift in regulatory mood. But unlike 2002, today’s environment is shaped by piecemeal rulemaking, stakeholder pressure, and global alignment (e.g., EU Corporate Sustainability Reporting Directive). This makes tracking developments more complex—but also more essential.

Compliance leaders should view the current moment not as a compliance cliff, but as a slope—one that’s becoming steeper, faster, and more technical. Keeping ahead means distinguishing hard rules from noisy headlines, and planning accordingly.

5. Breakdown of New Compliance Demands

Though there is no single “SOX 2.0” statute, the compliance landscape is being reshaped by a series of rulemakings, expectations, and emerging standards that, together, demand a broader and deeper organizational response. These shifts are not simply about ticking new boxes—they are recalibrating how organizations define material risk, manage controls, and document accountability.

1. Disclosure Requirements: Beyond Financials

New compliance expectations are expanding disclosures into non-financial domains. Companies must now address operational vulnerabilities, reputational risks, and environmental exposure in their public filings.

- Cybersecurity (SEC Final Rule, 2023):

Companies are required to disclose material cybersecurity incidents within four business days and provide detail on risk management, strategy, and board oversight. This effectively elevates cyber governance to the same level as financial controls. - Climate Risk (Pending Finalization):

The proposed SEC rule would compel large filers to disclose:- Scope 1 and 2 greenhouse gas emissions (Scope 3 in some cases)

- Climate-related governance structures

- Transition risks and resilience strategies

This moves environmental strategy into the realm of financial risk, placing CFOs and controllers in unfamiliar territory.

- AI/Automated Systems:

While not yet regulated explicitly, early guidance suggests that disclosures on how AI systems affect decision-making, fairness, and risk controls may soon become standard, especially in sectors like finance, insurance, and e-commerce.

2. Risk Management Expansions

Compliance is becoming synonymous with enterprise risk management (ERM). Regulators increasingly expect companies to demonstrate integrated governance, particularly in areas traditionally outside the purview of SOX.

- Cybersecurity risk mapping

- Third-party/vendor risk due diligence

- Climate scenario planning

- AI model governance and auditability

These aren’t just technical exercises; they require board-level involvement and real-time monitoring systems.

3. Internal Controls: Reimagined for the Digital Age

Internal controls over financial reporting (ICFR) are still a regulatory centerpiece—but now, organizations are being nudged to adopt Internal Controls over Non-Financial Reporting (ICONFR).

Emerging best practices include:

- Integrated dashboards for ESG and financial metrics

- Real-time alerts on data anomalies (e.g., emissions overages or supply chain lags)

- Inclusion of cyber resilience metrics in IC reviews

- AI-assisted audit trails

Some firms are piloting “controls-as-code” systems where policy enforcement is embedded directly into IT architecture—something unthinkable under the 2002 compliance paradigm.

4. Audit Committee Expansion

Audit committees, once guardians of financial accuracy, are increasingly being tasked with oversight of climate, cyber, AI ethics, and even social governance. The skills required are changing, and many boards are reshuffling to include technologists and risk strategists.

Key changes include:

- Expanded charters to include tech and sustainability oversight

- Cross-functional alignment with IT, legal, and sustainability teams

- New benchmarks for audit committee performance tied to risk event outcomes

5. Technology and Real-Time Compliance

One of the most transformational changes is the shift toward real-time, tech-enabled compliance. This includes:

- Continuous monitoring systems for key risk indicators

- Automated control testing and reporting

- Regulatory change management tools

- Use of machine learning to detect policy violations or reporting anomalies

Manual quarterly checklists are being replaced with automated compliance pipelines that mirror the speed of today’s operational environments.

Visual: Layered Compliance Domain Matrix

Below is a matrix that illustrates how traditional SOX domains are being expanded or redefined by current regulatory and market shifts.

| Domain | Then (SOX 2002) | Now (Evolving 2025) |

|---|---|---|

| Financial Reporting | Income statements, balance sheets | ESG metrics, AI-driven outputs, integrated disclosures |

| Internal Controls | ICFR (Internal Control over Financial Reporting), manual testing | ICONFR (Internal Control over Non-Financial Reporting), real-time risk monitoring |

| Executive Oversight | CEO/CFO certification under Sections 302 & 906 | Broader risk ownership, oversight of ESG, cyber, AI |

| Audit Function | External audits focused on financial accuracy | Integrated audits covering cyber, ESG, operational data |

| Disclosure Scope | Historical reporting (10-K, 10-Q) | Forward-looking risk disclosures (climate, cyber, etc.) |

This new compliance architecture isn’t just bigger—it’s more interconnected. Financial, operational, environmental, and reputational risks are now being treated as a single ecosystem. Companies that silo governance into old categories may find themselves out of step with both regulators and markets.

6. Impact on Companies: What’s Changing in Practice

The evolving compliance landscape is already reshaping how companies operate day to day. From governance structures to technology investment, the pressure to meet new standards—some formalized, others emerging—has forced organizations to rethink their internal architecture. The response varies by sector and size, but across the board, forward-leaning companies are moving away from static compliance checklists toward integrated, risk-aware governance ecosystems.

Below are snapshots of how several leading firms are adapting in practice.

Vignette 1: Microsoft – Board-Level Cyber Accountability

In 2023, Microsoft publicly overhauled its board-level cybersecurity oversight. Following multiple high-profile nation-state intrusions, the company established a dedicated Cybersecurity & Technology Risk Committee reporting directly to the board. This new body oversees data governance, product security practices, and third-party risk across the enterprise.

In parallel, Microsoft shifted some CISO reporting lines to create cross-functional integration with legal, compliance, and finance—a move that reflects how cybersecurity is now viewed not just as an IT problem, but a material business risk with regulatory and reputational implications.

Lesson: Cyber risk isn’t just an operational concern—it’s now central to board governance, especially for systemically important technology firms.

Vignette 2: Salesforce – ESG Controls and Disclosure Integration

Salesforce, a vocal proponent of stakeholder capitalism, has taken a proactive stance on ESG reporting. Even ahead of formal SEC requirements, the company aligned its ESG disclosures with TCFD (Task Force on Climate-Related Financial Disclosures) and SASB (Sustainability Accounting Standards Board) frameworks. It also began integrating these metrics directly into its SOX controls environment.

Notably, Salesforce partnered with its internal audit team to apply “controls logic” to climate data—treating emissions reporting and supplier metrics with the same rigor traditionally reserved for revenue or liabilities.

Lesson: Treating ESG data with financial-grade discipline is becoming a differentiator—and a hedge against future regulatory tightening.

Vignette 3: JPMorgan Chase – AI Governance and Model Risk Management

In the finance sector, JPMorgan Chase has led in developing internal controls over the use of AI and machine learning in credit, fraud detection, and trading. The bank’s Model Risk Management (MRM) framework, initially developed for stress testing and regulatory capital models, has expanded to include algorithmic bias monitoring and explainability standards for AI-based decisions.

JPMorgan’s governance approach treats AI models like other high-risk financial systems: they are version-controlled, independently validated, and subject to audit. Importantly, this framework is now referenced in analyst calls and shareholder disclosures—a signal of its perceived materiality.

Lesson: AI oversight is not a future issue—it’s already being regulated through existing risk management expectations.

Common Themes Across Organizations

Despite differences in sector and scale, the leading organizations responding well to emerging compliance demands share a few key characteristics:

- Proactive Framing

They don’t wait for regulations to be finalized. Instead, they anticipate and act on regulatory direction, building systems that align with the most stringent global expectations. - Cross-Functional Integration

Compliance is no longer the domain of siloed departments. Risk, legal, IT, sustainability, finance, and operations increasingly collaborate to ensure controls and reporting are holistic. - Technology-Driven Compliance

Manual processes are giving way to automation, continuous control monitoring, and dashboards that track key risk indicators in real time. - Cultural Shift

At these firms, compliance isn’t seen as overhead—it’s tied to brand trust, investor confidence, and strategic positioning.

The bottom line? Leading companies aren’t waiting for a legislative hammer to fall. They’re acting on the understanding that risk—especially reputational and technological—is now compliance-relevant even before it becomes codified in law.

7. Legal and Ethical Implications for Executives

As compliance expectations expand beyond financial disclosures into ESG, cyber risk, and AI governance, executive liability is entering new territory. The spirit of Sarbanes-Oxley was always about accountability at the top—and now that ethos is being applied to a much wider set of disclosures and decisions.

Personal Liability: Echoes of Section 302/906

Under SOX, Sections 302 and 906 mandated that CEOs and CFOs personally certify the accuracy and completeness of financial reports, under penalty of civil and criminal consequences. Today, similar scrutiny is beginning to form around non-financial risks. The SEC has made it clear that climate or cyber disclosures, if deemed materially misleading, could carry the same weight as financial misstatements.

Executives may not yet be signing ESG disclosures with a 906-style attestation, but legal observers warn: it’s only a matter of time. The precedent has been set.

Tone at the Top: Expanded Ethical Leadership

“Tone at the top” has long been a key principle in governance—but the definition of ethical leadership is evolving. It now includes:

- Proactive governance over tech and AI use

- Clear accountability structures for sustainability promises

- Whistleblower-friendly cultures with internal escalation pathways

Executives who delegate compliance to isolated departments without proper board oversight or cross-functional integration are increasingly seen as negligent—even if unintentional.

Whistleblower Protections and Retaliation Risks

The SEC’s whistleblower program continues to grow in scope and impact. In 2023 alone, the agency awarded over $600 million to individuals whose tips led to enforcement actions. Companies that suppress or retaliate against internal dissent, especially in areas like ESG or cybersecurity misreporting, face both legal and reputational blowback.

The message is clear: the modern executive is expected not only to lead ethically, but also to be deeply informed across a growing matrix of operational, technological, and societal risks. The line between oversight and liability has never been thinner.

8. Strategic Response: What Companies Should Do Now

For compliance leaders, board directors, and executives, the question is no longer if new mandates are coming—but how to prepare for them amid uncertainty. The regulatory path may be fragmented, but the direction is clear: more transparency, more accountability, and more scrutiny of non-financial risk.

Companies that wait for finalized rules or legislation will find themselves reacting late, retrofitting systems under pressure. By contrast, leading organizations are building future-ready compliance architectures now—flexible enough to absorb evolving expectations and rigorous enough to withstand enforcement.

Below is a strategic response framework for companies aiming to stay ahead of the SOX 2.0 curve:

✅ Strategic Compliance Roadmap

1. Conduct a Gap Assessment

- Map current compliance systems against proposed and anticipated regulatory domains (climate, cyber, AI, ESG).

- Identify where existing SOX controls can be leveraged or extended.

- Involve finance, legal, IT, sustainability, and operations to ensure a 360° view.

2. Modernize Risk and Control Frameworks

- Shift from static, point-in-time control reviews to continuous control monitoring (CCM).

- Use controls-as-code or automation to scale with complex data streams (e.g., real-time emissions tracking, AI model logs).

- Integrate ESG, cyber, and operational risk into enterprise risk management (ERM) systems.

3. Enhance Governance and Oversight

- Expand audit committee or form subcommittees for cyber and sustainability oversight.

- Assign clear executive ownership for each disclosure domain (e.g., CISO for cyber risk governance).

- Train board members on evolving areas of material risk (AI bias, climate liability, etc.).

4. Engage Regulators and Industry Coalitions

- Participate in comment periods and public forums hosted by the SEC, PCAOB, or FASB.

- Benchmark practices against peer disclosures and standards (e.g., TCFD, NIST, SASB).

- Join cross-industry groups to shape consensus around emerging best practices.

5. Prioritize Talent and Culture

- Upskill compliance, internal audit, and risk teams on data science, sustainability, and technology governance.

- Foster a culture where transparency and ethics are championed—not feared.

- Ensure whistleblower channels are visible, trusted, and used constructively.

In this environment, resilience is the new compliance standard. Companies that treat this moment as an opportunity to rebuild smarter, rather than bolt on patches, will be best positioned—regardless of whether “SOX 2.0” becomes law in name or just in nature.

9. Conclusion: The Road Ahead — Evolution or Revolution?

While “SOX 2.0” may never materialize as a single piece of sweeping legislation, its spirit is already reshaping corporate compliance. The shift underway is both evolutionary and revolutionary: evolutionary in its reliance on expanded interpretations of existing frameworks, revolutionary in its scope across technology, climate, and governance.

The smartest companies aren’t asking whether these changes are real—they’re preparing for them. By embedding transparency, cross-functional oversight, and technology-driven controls into their DNA, they’re not just staying compliant. They’re building resilience.

In an age where trust is currency, compliance is no longer just a safeguard—it’s a strategic asset.