In 2025, the U.S. Securities and Exchange Commission (SEC) unveiled one of its most comprehensive overhauls to financial regulation in decades—introducing a new rulebook that redefines the compliance landscape for accountants. This rulebook reflects a shift toward enhanced transparency, real-time data reporting, and accountability across both public and private sectors. For accounting professionals, especially those in advisory and audit roles, the changes are far-reaching: from ESG disclosure standards and cyber-risk reporting to tightened internal control frameworks and digital-first compliance mandates.

This article breaks down the key regulatory updates with a focus on their practical implications for CPAs and accounting firms. Whether you’re leading a reporting team, advising clients, or navigating new assurance expectations, understanding the SEC’s 2025 framework is critical. This is more than a compliance update—it’s a strategic inflection point for the profession. The following sections provide a step-by-step roadmap to help you prepare, adapt, and lead in this evolving environment.

Introduction: A Regulatory Turning Point

The landscape of financial regulation has never stood still, but 2025 marks a particularly pivotal year. The SEC’s release of its updated rulebook isn’t merely a routine refresh—it represents a deliberate pivot toward modernized oversight, accelerated by rapid technological advancement, increased investor scrutiny, and heightened global alignment pressures. For seasoned accountants, this isn’t just another update to track; it’s a signal of broader institutional change.

Over the past decade, the role of financial professionals has expanded beyond traditional reporting. Today, accountants are expected to interpret regulatory language, manage risk, assure integrity in data systems, and increasingly, weigh in on non-financial metrics like sustainability and cybersecurity. The SEC’s new framework acknowledges this evolution and seeks to codify new standards that reflect the modern realities of capital markets.

This article aims to decode the rulebook through a professional lens. While some changes build upon familiar principles, others demand a recalibration of long-standing processes and assumptions. If you’re in public practice, corporate finance, or advisory, understanding what’s changed—and why—will be crucial to guiding your organization or clients through this regulatory shift.

Overview of the SEC’s New Rulebook

The SEC’s 2025 rulebook is not just a revision; it’s a structural reimagining of how regulatory guidance is organized, interpreted, and enforced. Designed to bring clarity, consistency, and forward compatibility, the new framework is organized into five core pillars:

- Modernized Financial Reporting

- Enhanced Governance and Internal Controls

- Mandatory ESG Disclosures

- Cybersecurity and Technology Risk Reporting

- Digital Filing and Automation Standards

Each pillar is designed to align more closely with evolving stakeholder expectations, international standards, and the digital infrastructure of today’s businesses. The rulebook introduces streamlined taxonomy, eliminates redundant or obsolete provisions, and enhances guidance clarity through integrated commentary and interpretive notes.

A notable shift is the SEC’s embrace of principles-based language in certain areas—especially ESG reporting—moving away from overly prescriptive metrics toward materiality-driven disclosures. At the same time, more stringent rules now apply to financial reporting controls, requiring deeper documentation of risk assessments and validation processes.

One of the most transformative aspects of the new rulebook is its modular structure, which allows the Commission to issue real-time updates via designated appendices without requiring full rewrites. This “living framework” anticipates a faster regulatory feedback loop, where evolving risks (like AI misuse or geopolitical cyber threats) can be addressed swiftly through targeted guidance.

Another key innovation is the integration of cross-referenced compliance maps—visuals that help professionals quickly locate interrelated requirements across different sections. These diagrams (which firms may wish to replicate internally) improve audit planning and reduce the risk of overlooked obligations.

Finally, the rulebook provides clearer delineation of auditor versus management responsibilities. This is critical, particularly in high-risk areas such as internal controls over financial reporting (ICFR) and emerging ESG disclosures.

In summary, the 2025 rulebook is more than a compliance document—it’s a strategic blueprint. For accountants, early mastery of its structure and themes is essential not only for compliance but for enabling proactive business guidance.

Major Updates Relevant to Accountants

The 2025 SEC rulebook introduces sweeping changes that directly impact how accountants approach financial reporting, assurance, and compliance. While some updates build on existing frameworks, others signal a major shift in expectations for documentation, professional judgment, and interdisciplinary collaboration. Below are the most critical updates accounting professionals need to understand.

1. Financial Reporting and Disclosure Reforms

The SEC has redefined several key financial reporting obligations, with a focus on real-time transparency and comparability across registrants:

- Quarterly and Annual Report Enhancements: Registrants must now provide more granular breakdowns of revenue recognition, contingent liabilities, and segment disclosures. The rulebook outlines standardized data fields, reducing subjectivity in interpretations.

- Restatement Protocols: The criteria for identifying and disclosing material errors have been tightened. Accountants must document more robust justification for restatements, including supporting analytics and audit trail validation.

- Use of Estimates: Enhanced disclosure requirements now require explanation of methodology, not just estimate values. This affects areas such as fair value measurements, credit loss provisioning (CECL), and asset impairments.

2. Internal Controls Over Financial Reporting (ICFR)

Accountants, especially auditors and CFO teams, will feel a significant shift in expectations around internal controls:

- Risk-Weighted Documentation: Control documentation must now align with a risk-based scoring model. Controls over high-risk areas (e.g., revenue, cybersecurity) require more frequent testing and multi-layer documentation.

- Automation and Controls: The SEC now expects filers to explicitly disclose and evaluate the controls embedded in automated workflows and AI-assisted processes.

- Sub-Certification Requirements: Larger registrants must obtain sub-certifications from process owners, adding a second layer of accountability to management’s attestation.

3. ESG Reporting Integration

Perhaps the most debated section of the new rulebook is the mandatory ESG disclosure framework. Though principles-based in nature, it requires accountants to step into new territory:

- Climate Risk and Carbon Disclosures: Companies must now report Scope 1 and Scope 2 emissions, with Scope 3 disclosures mandated for certain industries. Accountants must assess whether controls exist over the underlying data, often coming from outside finance.

- Governance Reporting: Disclosure of board-level ESG oversight, executive incentive alignment, and sustainability risk factors is now required.

- Assurance Over ESG Metrics: While not mandatory, the SEC strongly encourages third-party assurance of ESG data. Accountants may find themselves providing limited assurance or advising clients on control readiness for future audits.

4. Audit Committee and Auditor Communication

The rulebook codifies expanded expectations for auditor communication with audit committees, particularly regarding emerging risks:

- Materiality Thresholds: Auditors must justify how thresholds are applied differently for financial vs. non-financial data, especially under ESG reporting.

- Critical Audit Matters (CAMs): CAM reporting has been expanded to include forward-looking risk disclosures and technology-enabled audit evidence.

5. Real-Time Reporting and Event Triggers

New “Event-Driven Disclosure” rules mandate rapid reporting of specific events, many of which require immediate accountant involvement:

- Cybersecurity breaches

- Significant vendor or third-party failures

- Major changes in capital structure or financing terms

These rules compress the timeline for financial analysis and require standing protocols for rapid materiality assessment.

| Area | Old Rule | New Rule (2025) | Accountant’s Responsibility |

|---|---|---|---|

| Financial Reporting | Broad reporting categories; more flexibility in disclosures. | Granular breakdowns, standardized formats (e.g., segment data, estimates). | Adjust reporting templates, ensure detailed footnotes, validate disclosure accuracy. |

| Internal Controls (ICFR) | Management-level attestation with basic documentation. | Risk-weighted documentation, automation review, sub-certifications required. | Expand testing, enhance documentation, guide process owners on control quality. |

| ESG Disclosures | Voluntary, fragmented ESG reporting with no standard framework. | Mandatory Scope 1 & 2 disclosures; board oversight reporting; encourage assurance. | Advise on ESG metrics, assess data controls, prepare for future assurance engagements. |

| Cybersecurity Reporting | General risk discussion in MD&A. | Specific incident disclosure within 4 business days; governance structure required. | Collaborate with IT/legal on disclosure triggers, support governance documentation. |

| Audit Committee Communication | Periodic reporting of material issues. | Broader CAM scope including emerging risks and audit methodology. | Communicate forward-looking risk factors, expand CAM reporting scope, document audit strategy. |

| Digital Filing (iXBRL) | Limited to financial statements. | Full iXBRL tagging including MD&A, ESG, and governance sections. | Coordinate taxonomy updates, validate tagged data, test filing integrity. |

| Automation & AI | Not explicitly addressed in controls frameworks. | Controls required over AI models, algorithmic logic, and data pipelines. | Review digital processes, test logic validity, ensure outputs align with GAAP principles. |

| Non-Financial Metrics | Not mandatory; disclosed at discretion. | Required disclosure of material non-financial KPIs (e.g., workforce, carbon). | Verify KPI data, review sources, assess integration into financial narrative. |

| Event-Based Reporting | 8-K or similar reports filed within longer windows (up to 10 days). | Certain events now require disclosure within 4 business days. | Build rapid assessment protocols, maintain pre-approved language templates. |

| Third-Party Risk Oversight | Minimal disclosures around outsourced functions. | Disclosure of material vendor risks, including cloud and service providers. | Conduct vendor control evaluations, ensure SOC reports are current and reviewed. |

| Auditor Independence & Ethics | Standard independence declarations; annual conflict check. | Enhanced scrutiny on dual roles, ESG advisory overlap, and independence boundaries. | Update conflict-check protocols, reassess service lines offered, re-educate staff on boundaries. |

In sum, the 2025 rulebook redefines the accounting function—not just as a compliance enabler, but as a risk strategist, ESG advisor, and digital control architect. Professionals who understand the depth of these changes will be best positioned to lead rather than react.

Technology and Digital Compliance

The SEC’s 2025 rulebook brings digital compliance into the regulatory spotlight, introducing concrete mandates that redefine how accountants manage and communicate data. For professionals accustomed to traditional reporting cycles and manual processes, these changes signal a fundamental shift in practice.

1. XBRL and Inline XBRL (iXBRL) Expansion

While structured data reporting is not new, the new rulebook requires full-scope iXBRL tagging across virtually all narrative sections of filings—not just financial statements. This includes:

- Management’s Discussion and Analysis (MD&A)

- ESG disclosures

- Risk factors and governance commentary

Accountants must now work closely with IT and reporting teams to ensure consistent, accurate tagging and to verify taxonomy mapping aligns with the SEC’s expanded digital schema.

2. Cybersecurity Disclosure Requirements

The rulebook introduces a dedicated cybersecurity disclosure standard. Companies must now:

- Report material cyber incidents within four business days of identification.

- Disclose their cyber risk governance structure, including board oversight and internal control frameworks.

- Detail third-party exposure, particularly in relation to service providers or outsourced financial systems.

For accountants, this means expanded collaboration with CISOs and legal counsel to assess and document materiality thresholds, financial exposure, and disclosure timing.

3. Data Governance and Automation Oversight

Automated processes—particularly those involving AI or machine learning—are now subject to internal control review. This includes:

- Validating the accuracy and integrity of source data used in automated financial systems.

- Ensuring algorithmic decision-making tools don’t introduce bias or violate GAAP principles.

- Documenting controls over data lineage and audit trails.

The message is clear: accountants must now think like digital custodians. Mastering structured data and digital compliance is no longer optional—it’s central to maintaining regulatory credibility.

Implications for Public Companies vs. Private Entities

While the SEC’s rulebook primarily governs publicly traded companies, its ripple effects will be felt across the private sector as well. The 2025 updates introduce nuanced distinctions in how rules are applied—but also where alignment is encouraged or expected. For accountants, understanding these differences is critical for appropriately advising clients or managing internal compliance efforts.

1. Public Companies: Full Scope Compliance

Public companies face the full weight of the rulebook, with mandatory adherence to all five regulatory pillars. This includes:

- Complete iXBRL integration across all filings

- ESG disclosures in 10-Ks and 10-Qs

- Real-time event-based reporting within shortened windows

- Expanded ICFR documentation and attestation

For accounting teams, this means deeper coordination with internal audit, legal, and investor relations. The increased scrutiny from analysts, regulators, and proxy advisors further elevates the risk of noncompliance.

2. Private Entities: Voluntary Adoption and Market Pressures

While private companies are not legally bound by many of the new SEC rules, they are indirectly affected in three key ways:

- Investor and lender expectations: Banks, VCs, and PE firms increasingly require ESG reporting, robust controls, and cyber-risk disclosures.

- IPO readiness: Companies planning to go public must build SEC-aligned frameworks well in advance.

- Audit and advisory pressure: Accounting firms are encouraging private clients to adopt elements of the new rulebook proactively, especially for ESG and internal controls.

💡 Tip for CPAs: Develop differentiated checklists and templates for public vs. private clients to ensure scalable compliance planning.

Role of the CPA in Navigating Compliance

The SEC’s 2025 rulebook does more than redefine reporting requirements—it redefines the role of the accountant. CPAs are no longer just stewards of financial accuracy; they are now central figures in governance, risk, sustainability, and digital oversight. For professionals across public accounting and corporate finance, this means adopting a broader, more strategic mindset.

1. Evolving Advisory Responsibilities

The regulatory emphasis on principles-based disclosure—especially in ESG and cyber domains—requires CPAs to apply professional judgment in areas where metrics are less defined. This blurs the lines between financial and non-financial advisory.

- Materiality interpretation for ESG risks

- Advising boards on internal control frameworks

- Helping clients benchmark disclosures against peers or industry norms

CPAs must now understand the regulatory environment holistically to provide relevant, actionable insights.

2. Assurance Adaptations

The expansion of required disclosures has direct implications for audit procedures:

- Enhanced testing of non-traditional data (e.g., carbon emissions, supply chain disruption impacts)

- Scrutiny over automated workflows and AI-driven calculations

- More rigorous documentation and evidence gathering, especially around internal control environments

Expect audit planning to include expanded involvement from IT specialists and forensic teams to validate control integrity across digital systems.

3. Ethical and Legal Implications

With faster reporting deadlines and real-time event triggers, the pressure to make materiality judgments quickly has increased. CPAs must be vigilant in upholding:

- Independence and objectivity, especially when advising clients while also offering assurance

- Due care and diligence, in rapidly evolving reporting situations

- Ethical boundaries, especially when facing client resistance to disclosures that may impact valuation or perception

Firms should invest in regular ethics refreshers tied specifically to regulatory interpretation and emerging risk areas.

📘 Pro Tip: CPAs should actively participate in interdisciplinary compliance committees—combining finance, legal, IT, and sustainability functions—to stay aligned and influential.

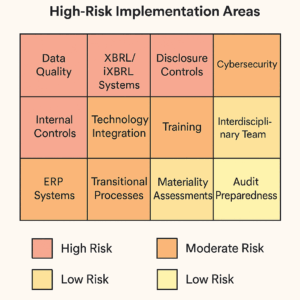

Implementation Challenges and Practical Considerations

Adopting the SEC’s 2025 rulebook isn’t a matter of flipping a switch. For most organizations, the transition will require sustained effort across systems, teams, and culture. Accountants sit at the intersection of these moving parts and are uniquely positioned to lead the implementation—but not without challenges.

1. Compressed Timelines and Transitional Burden

Although the SEC has provided a phased compliance timeline for some provisions, several key requirements—such as cybersecurity incident reporting and expanded XBRL—take effect in 2025. This leaves limited runway for companies to:

- Rework internal controls documentation

- Train staff on new disclosure standards

- Update ERP and reporting platforms to support structured data and automation

Accountants must balance these tasks against ongoing audit cycles and reporting deadlines, creating a resource strain for lean finance teams.

2. Systems Integration and Technology Gaps

The rulebook assumes a level of digital maturity many mid-market and private companies lack. Integrating ESG data, automating XBRL tagging, or tracking cyber incidents in real time requires system upgrades and cross-department coordination. Accountants may need to act as bridge-builders between finance, IT, and operations to define data flows and controls.

3. Talent and Training Constraints

The shift toward digital compliance and non-financial reporting exposes a skills gap in many accounting departments. ESG literacy, data analytics, and familiarity with cloud-based audit tools are now essential competencies—but not yet standard. Firms that fail to upskill may find themselves reactive rather than strategic.

In short, accountants must manage the friction of change while ensuring no regulatory detail is missed. The challenge is real—but so is the opportunity to elevate the profession’s influence.

What Firms Should Do Now: Strategic Recommendations

With the SEC’s 2025 rulebook officially in effect, the clock is ticking. Compliance isn’t just about checking boxes—it’s about embedding sustainable practices that will hold up under scrutiny from regulators, investors, and auditors. The most successful firms will treat this moment as a strategic inflection point, not a technical headache.

Below are five practical, high-impact actions accountants and firms should prioritize now.

1. Perform a Readiness Assessment

Start with a diagnostic of your current compliance posture. Map your organization’s existing disclosures, internal controls, ESG data collection, and cyber protocols against the new rulebook. Identify gaps, overlaps, and areas of high exposure.

- Tip: Use cross-functional workshops to ensure you’re not siloed in your analysis.

2. Invest in System Upgrades and Process Automation

Modernized reporting demands digital agility. Firms should prioritize:

- iXBRL-enabled reporting tools

- Real-time disclosure tracking systems

- Integrated ESG and financial data platforms

The goal isn’t just compliance—it’s building efficiency and auditability into your workflows.

3. Train and Upskill Staff

Develop tailored training for finance, audit, and compliance teams. Topics should include:

- ESG disclosure mechanics

- Digital controls over AI/automation

- SEC event-driven reporting standards

Encourage CPE programs that blend accounting with data governance, ethics, and regulatory interpretation.

4. Formalize Interdisciplinary Governance

Create or reinforce a governance committee that includes finance, legal, IT, and sustainability leads. This structure supports unified responses to rapid-reporting requirements and improves risk oversight.

5. Engage External Advisors Proactively

Don’t wait for an SEC comment letter. Collaborate now with auditors, legal counsel, and ESG specialists to validate assumptions, fine-tune disclosures, and pressure-test controls.

Looking Ahead: The Evolving Role of Regulation

While the 2025 rulebook represents a major regulatory milestone, it is by no means the final word. The SEC has signaled that this framework is designed to evolve, with future updates anticipated in areas such as artificial intelligence governance, digital asset disclosures, and cross-border data transparency.

Global convergence is another key theme. Expect further harmonization between SEC standards and international frameworks like IFRS Sustainability Disclosure Standards (IFRS S1/S2) and E.U. CSRD regulations. For multinational companies—and the firms that support them—this alignment means more integrated reporting and assurance expectations worldwide.

For accountants, the future will demand more than technical fluency. The profession is being called to act as an ethical compass, a technology translator, and a strategic advisor. The SEC’s shift is not simply regulatory; it’s cultural. Staying ahead means staying adaptable—and deeply informed.

Conclusion

The SEC’s 2025 rulebook signals more than a regulatory overhaul—it marks a redefinition of the accounting profession’s role in financial integrity, risk governance, and strategic disclosure. For CPAs, it’s a call to evolve: to lead conversations on ESG, ensure digital trust, and navigate complexity with foresight and precision. Compliance is no longer a reactive task—it’s a proactive, cross-functional discipline. As the regulatory landscape continues to shift, those who embrace these responsibilities early will shape not just reports—but reputations, markets, and decision-making itself. Now is the time to lean in.