1. Introduction: Framing the Debate

Private equity (PE) has long been known for its disruptive impact on industries ranging from retail to healthcare. But its foray into the accounting profession—an arena historically guarded by conservative structures and regulatory oversight—has stirred a new wave of scrutiny. What happens when firms that prize transparency and independence fall under the influence of capital owners who prioritize returns?

Over the past few years, private equity firms have acquired or taken substantial stakes in accounting practices, reshaping ownership models that were, for decades, dominated by partnerships rooted in professional ethics rather than investor ROI. This shift is more than cosmetic—it challenges the very fabric of how trust is built in financial reporting.

Is this a long-overdue modernization, injecting capital, technology, and business rigor into a profession ripe for evolution? Or does it threaten the independence and credibility of auditors and advisors, raising questions about conflicts of interest, governance, and long-term accountability?

This article unpacks the motivations behind PE’s growing presence in accounting, the risks it introduces, and the evolving response from regulators and industry leaders. It’s a critical conversation—one that could redefine the future of financial assurance in the global economy.

2. Historical Context: Accounting Firms and Ownership Models

For most of their modern existence, accounting firms have adhered to a partnership model that emphasizes professional stewardship over commercial gain. This structure—where ownership is restricted to licensed professionals—has long been viewed as essential to maintaining auditor independence and public trust. The logic was simple: those tasked with providing assurance to capital markets must be insulated from undue financial influence themselves.

Globally, this ethos was embedded in regulation. In the U.S., the Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board (PCAOB) mandate strict rules around audit independence. Internationally, bodies like IFAC (International Federation of Accountants) and country-specific regulators reinforced these boundaries. Ownership and governance structures were not just internal decisions; they were policy issues tied to public interest.

However, pressures on the traditional model began to mount in the 2000s. Rising costs, technological change, and consolidation in the corporate world drove many mid-sized firms to seek outside capital to remain competitive. Some jurisdictions, such as the U.K. and Australia, relaxed ownership restrictions, opening the door—albeit cautiously—to non-accountant investors.

Still, private equity remained largely on the sidelines until recently. What has changed isn’t just market conditions—it’s the growing belief that the accounting profession, once deemed off-limits to outside capital, may now be both vulnerable and valuable.

3. Private Equity’s Entry into the Accounting Sector

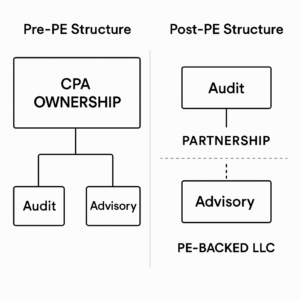

Private equity’s presence in accounting is no longer theoretical—it’s actively reshaping the industry. In recent years, a growing number of accounting firms, particularly in the mid-market, have accepted private equity investment, often through complex restructuring. These deals typically involve the formation of new corporate entities, allowing for PE ownership while maintaining technical compliance with regulatory independence rules.

One of the most cited examples is EisnerAmper, a top 20 U.S. accounting firm, which in 2021 announced a landmark deal with TowerBrook Capital Partners. The firm split into two entities: one providing attest services (which remains a CPA-owned partnership), and another offering advisory services—where TowerBrook took a significant equity stake. The structure created a firewall to meet independence requirements while injecting substantial growth capital into EisnerAmper’s advisory arm.

Similar models have emerged across the U.S. and U.K. In 2022, Parthenon Capital invested in RSM US’s consulting business. In 2023, Grant Thornton UK explored spinning off its non-audit services into a PE-backed entity. These transactions signal a trend: private equity isn’t buying entire firms outright, but rather carving out lucrative segments—particularly in tax, advisory, and consulting—where independence rules are less stringent.

What’s driving this wave of deals? For PE firms, accounting represents a stable, cash-generating business with built-in client relationships and cross-selling potential. For accounting firms, the motivations are equally pragmatic: capital for acquisitions, talent retention strategies, IT modernization, and the ability to compete with larger networks like the Big Four.

But the implications are far-reaching. These hybrid ownership models blur the lines between professional service and commercial enterprise. As more firms adopt dual-entity structures, questions arise about whether audit independence can be sustained in an environment where adjacent business units are profit-maximized by third-party investors.

4. Opportunities: Capital, Innovation, and Modernization

While skepticism around private equity’s motives in professional services is warranted, it’s equally important to acknowledge the real opportunities this shift introduces—particularly in a profession that has often lagged in technological adoption and structural flexibility.

The accounting industry has historically faced constraints in scaling, primarily due to its capital-light partnership model. For mid-tier firms, the barriers to investment in modern infrastructure—such as cloud platforms, cybersecurity, AI-driven audit tools, and client-facing digital portals—are substantial. Private equity changes that calculus. With external capital, firms are no longer limited to incremental, organic growth. They can invest aggressively in modernization, pursuing ambitious digital transformation agendas once exclusive to the Big Four.

Take EisnerAmper, for instance. Following its TowerBrook deal, the firm expanded its advisory services, launched new client technology platforms, and significantly broadened its industry footprint through acquisitions. Similarly, PE-backed firms now boast the resources to pursue mergers that create national or even global reach, challenging the incumbency advantage of legacy players.

Talent is another key driver. The profession has struggled to attract and retain younger professionals, particularly in advisory and consulting segments where competition with tech and finance firms is fierce. Private equity involvement allows accounting firms to offer more competitive compensation structures, equity incentives, and career advancement paths that mirror those in high-growth industries.

In addition, PE brings operational rigor. Many firms benefit from enhanced governance, performance metrics, and strategic clarity under PE stewardship. This can lead to better client outcomes, more data-driven decision-making, and a stronger institutional foundation.

Finally, private equity has a knack for unlocking value through specialization. By investing in niche verticals—such as forensic accounting, ESG advisory, or transaction services—PE-backed firms can dominate high-margin, high-growth segments that traditional firms have underserved.

None of this guarantees success, but it highlights why some in the profession view private equity as a catalyst for long-overdue evolution.

A before-and-after table showing improvements post-PE investment:

| Category | Traditional Model | Post-PE Model |

|---|---|---|

| IT Investment | Limited, incremental | Aggressive, transformative |

| Talent Strategy | Salary-based, rigid | Equity, performance-driven |

| Growth Model | Organic, conservative | M&A-driven, scalable |

| Advisory Focus | Limited scope | Specialized, tech-enabled |

5. Risks: Independence, Conflicts of Interest, and Governance

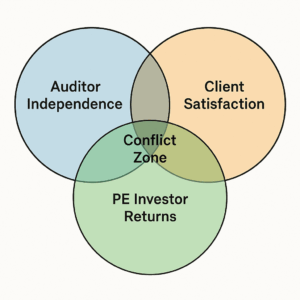

For all the strategic promise private equity brings to accounting firms, it also introduces a host of risks that cut to the heart of the profession’s credibility. Chief among these is the threat to auditor independence—the foundation on which public trust in financial reporting rests.

Accounting firms, particularly those offering audit services, are not just businesses; they are public interest entities. Their primary obligation is to provide objective assurance on financial information, even when it conflicts with the interests of their paying clients. The entry of private equity—whose mandate is inherently profit-maximizing—raises uncomfortable questions about whether these priorities can truly coexist.

Most PE transactions are structured to comply technically with independence rules. The audit function is typically ring-fenced in a CPA-owned entity, separate from the advisory arm where the PE firm holds its stake. But form does not always guarantee substance. Shared branding, overlapping leadership, joint marketing efforts, and integrated systems may compromise the perceived and actual independence of audit professionals. In a reputational profession like accounting, perception alone can erode trust.

There is also the issue of fiduciary duty. Managing partners in a PE-influenced structure are accountable not only to clients and regulators but also to private investors with defined exit timelines and return expectations. This can create a push toward short-term revenue maximization at the expense of long-term professional integrity. The temptation to cross-sell advisory services to audit clients—already a longstanding concern—is magnified under PE pressure.

Moreover, governance complexity increases. Traditional partnerships operate on consensus and professional judgment. PE-backed entities introduce boards, KPIs, return hurdles, and layered hierarchies that may dilute professional autonomy. Decision-making becomes more financialized, and less about stewardship or ethical risk management.

There’s precedent for concern. Past scandals—from Enron to Wirecard—highlight the catastrophic consequences when commercial interests outweigh professional duty. Introducing PE into this equation does not inherently cause such failures, but it undeniably raises the stakes.

Legal liability is another angle. If audit independence is compromised—whether in substance or appearance—regulators like the PCAOB or SEC may impose sanctions not just on firms, but potentially on their investors. The legal and reputational risk to PE firms themselves could become a deterrent, but until there is a clear regulatory stance, the gray area persists.

Finally, there’s the profession-wide impact. As more firms adopt PE-driven models, others may feel competitive pressure to follow suit just to stay viable. This could create a race to the bottom in governance and ethics, particularly among mid-sized firms that lack the institutional safeguards of the Big Four.

A Venn diagram illustrating overlapping interests and risks:

6. Regulatory and Professional Body Responses

The incursion of private equity into accounting has not gone unnoticed by regulators and professional bodies—though responses thus far have been fragmented, cautious, and in many cases, reactive rather than proactive.

In the United States, the Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board (PCAOB) have expressed increasing concern over the implications of complex ownership structures on auditor independence. While no explicit bans have been issued, regulatory rhetoric has sharpened. The PCAOB has emphasized that “technical compliance is not sufficient” and that firms must ensure that independence is upheld in both form and substance—a subtle but powerful warning to firms navigating these ownership transitions.

Elsewhere, the American Institute of Certified Public Accountants (AICPA) has largely focused on guidance, noting the need for member firms to maintain independence, transparency, and adequate disclosure, particularly in client engagement letters and public communications. However, as the AICPA has no enforcement authority over audit firms serving public companies, its role is more advisory than disciplinary.

Internationally, the picture is even more mixed. In the United Kingdom, the Financial Reporting Council (FRC) has expressed openness to external investment under strict conditions, especially for non-audit services, but has also launched consultations on firm governance and transparency. Australia, similarly, has permitted multidisciplinary firm structures that allow outside investment, albeit with requirements for professional control of audit functions.

What’s striking is the absence of a coordinated global framework addressing private equity investment in accounting. This leaves room for regulatory arbitrage—where firms exploit differences between jurisdictions to construct favorable ownership models that may comply locally but raise red flags globally.

There is growing momentum for stronger oversight. Industry voices and governance advocates are calling for clearer rules on PE investment, standardized disclosures of ownership structures, and perhaps even caps on investor influence in audit-related entities. Some have proposed a formal registry of PE-influenced firms, or mandatory reporting of internal governance mechanisms to regulators.

But until such measures are codified, the burden falls on firms to self-police—and on regulators to interpret outdated rules in a rapidly changing landscape.

Comparative Table: Regulatory Stances on Private Equity in Accounting

| Jurisdiction | Regulatory Body | Stance on PE Investment | Key Conditions / Concerns | Notable Developments |

|---|---|---|---|---|

| United States | SEC / PCAOB | Cautiously skeptical | Must preserve audit independence in substance, not just form | PCAOB has issued warnings; SEC monitors complex firm structures |

| United Kingdom | Financial Reporting Council (FRC) | Conditionally open | PE allowed in non-audit services; must maintain ethical walls | FRC launched consultation on governance and transparency |

| Australia | CA ANZ / ASIC | Permissive under structure | Allows multi-disciplinary partnerships; audit must remain under professional control | Several firms operate under mixed ownership models |

| Canada | CPAB / CPA Canada | Conservative | Emphasis on firm control by licensed professionals | Little PE activity observed; regulators monitoring developments abroad |

| European Union | Varies by country (e.g., AFM, BaFin) | Fragmented | Stricter in markets like Germany; more flexible in others | EU has no unified position; proposals emerging for audit reform post-Wirecard |

| International | IFAC | Neutral but cautious | Focuses on principles of independence and ethical conduct | Advocates global standards but lacks enforcement power |

7. Market Impact and Industry Reaction

Private equity’s growing presence in the accounting profession is not just a structural shift—it’s a market signal. For firms not yet engaged with outside capital, the trend introduces a new competitive reality, triggering both defensive and adaptive responses across the industry.

One of the most immediate effects has been on mid-tier and regional firms, which find themselves squeezed between the scale of the Big Four and the resource-rich agility of newly capitalized PE-backed competitors. These firms face pressure to either consolidate, specialize, or explore capital partnerships of their own. In some cases, talent poaching has accelerated, with PE-influenced firms able to offer more attractive compensation packages and faster career tracks, especially in advisory and consulting verticals.

Even among the Big Four, there is cautious attention. While these firms are unlikely to accept outside equity in their audit practices, they are investing heavily in internal venture funds, corporate spin-offs, and innovation hubs to maintain their edge. The growing legitimacy of private equity in professional services has, at a minimum, forced a cultural shift: one that values entrepreneurial thinking, productization of services, and revenue diversification.

For clients, the changes are both intriguing and unsettling. On the one hand, PE-backed firms may offer more responsive service models and innovative solutions. On the other, concerns about independence, continuity, and long-term firm stability have prompted some companies—particularly publicly listed ones—to revisit their audit provider criteria.

There’s also a branding evolution underway. Firms that were once seen as traditional and risk-averse are reintroducing themselves as dynamic, growth-oriented, and tech-forward. This shift can broaden appeal, but it may also dilute the profession’s core identity if not carefully managed.

Ultimately, private equity has not just entered the profession—it has begun to redefine the rules of engagement.

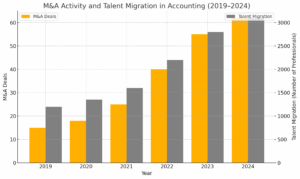

Here’s a bar graph illustrating the trends in M&A activity and talent migration within the accounting profession from 2019 to 2024. It highlights how both metrics have surged—particularly in the wake of private equity’s deeper engagement—indicating the profession’s ongoing structural and cultural transformation.

8. Outlook: Where Is This Headed?

The trajectory of private equity in accounting is still unfolding, but several trends are already taking shape. First, the dual-entity model—where audit and advisory are structurally separated—will likely become more common, particularly among mid-sized firms seeking capital without compromising regulatory compliance. This hybrid model allows firms to attract investment while navigating independence requirements, though it remains a delicate balancing act.

Second, we may see a wave of consolidation. Private equity firms are known for pursuing roll-up strategies—acquiring smaller players to create regional or national powerhouses. This could significantly reduce market fragmentation, especially in tax, advisory, and transaction services, where economies of scale improve margins and client delivery.

On the regulatory front, increased scrutiny and standardization are probable. Expect more defined global frameworks around ownership disclosure, governance, and independence safeguards—particularly as cross-border practices grow more complex.

Lastly, the profession itself may undergo a cultural transformation. As younger professionals enter firms shaped by investor logic and innovation-driven agendas, expectations around career mobility, firm loyalty, and ethical responsibility will shift. Whether this will strengthen or dilute the accounting profession’s identity remains an open—and critical—question.

What is clear, however, is that private equity’s presence is not a passing trend. It’s a structural evolution that’s only just beginning.

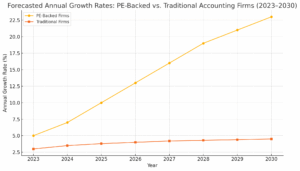

Here is the forecast chart comparing projected annual growth rates of PE-backed accounting firms versus traditional firms from 2023 to 2030. It highlights the more aggressive growth trajectory anticipated for PE-backed firms, largely due to M&A activity, capital infusion, and scaling strategies.

9. Conclusion: Balancing Innovation and Integrity

Private equity’s entry into the accounting profession is neither inherently good nor inherently dangerous—it is, instead, a powerful force that brings both promise and peril. On one hand, PE introduces long-needed resources for modernization, scalability, and competitiveness. It offers firms the means to transform digitally, attract top talent, and compete more effectively in a fast-changing advisory landscape.

But those advantages come with serious trade-offs. The accounting profession exists to safeguard the integrity of financial systems. That mission can only be fulfilled if independence, objectivity, and long-term trust are preserved—especially in audit services. Introducing profit-driven investors into that equation, without robust guardrails, raises unavoidable tensions.

The real question is not whether private equity should be involved in accounting, but how it can be involved without compromising the foundational principles of the profession. That answer will depend on thoughtful regulation, transparent firm governance, and a renewed commitment—by professionals and investors alike—to ethical stewardship.

As the profession evolves, the challenge will be to ensure that innovation doesn’t come at the cost of integrity. If done right, the future of accounting may well include private equity—but on terms that protect its public mission.